Editor’s Note: This analysis is part of the USC-Brookings Schaeffer Initiative for Health Policy, which is a partnership between Economic Studies at Brookings and the University of Southern California Schaeffer Center for Health Policy & Economics. The Initiative aims to inform the national health care debate with rigorous, evidence-based analysis leading to practical recommendations using the collaborative strengths of USC and Brookings. USC-Brookings Schaeffer Initiative research on surprise medical billing was supported by Arnold Ventures.

Air ambulances – which may be either helicopters or fixed-wing aircraft – provide medical transport for sick or injured patients from the scene of an accident or from one medical facility to another, and in recent years have garnered national attention for high and fast-rising prices. This rapid growth in air ambulance prices is borne by consumers both through higher insurance premiums and more directly through cost-sharing and surprise bills from out-of-network carriers. A recent study estimates that 40% of helicopter air ambulance rides result in a potential surprise bill averaging roughly $20,000.

Several analyses shed light on high and growing prices in the industry, but the concentration of high prices in a small number of private equity-owned carriers has not been as well explored. In this analysis, we utilize charge data submitted to Medicare and link carriers to their parent companies in order to examine billed charges by ownership structure over time. We report a standardized average charge for each carrier type that corresponds to an average distance transport to account for differences in the mix of services provided by carriers of different types. (See the Methodological Appendix for more detail.)

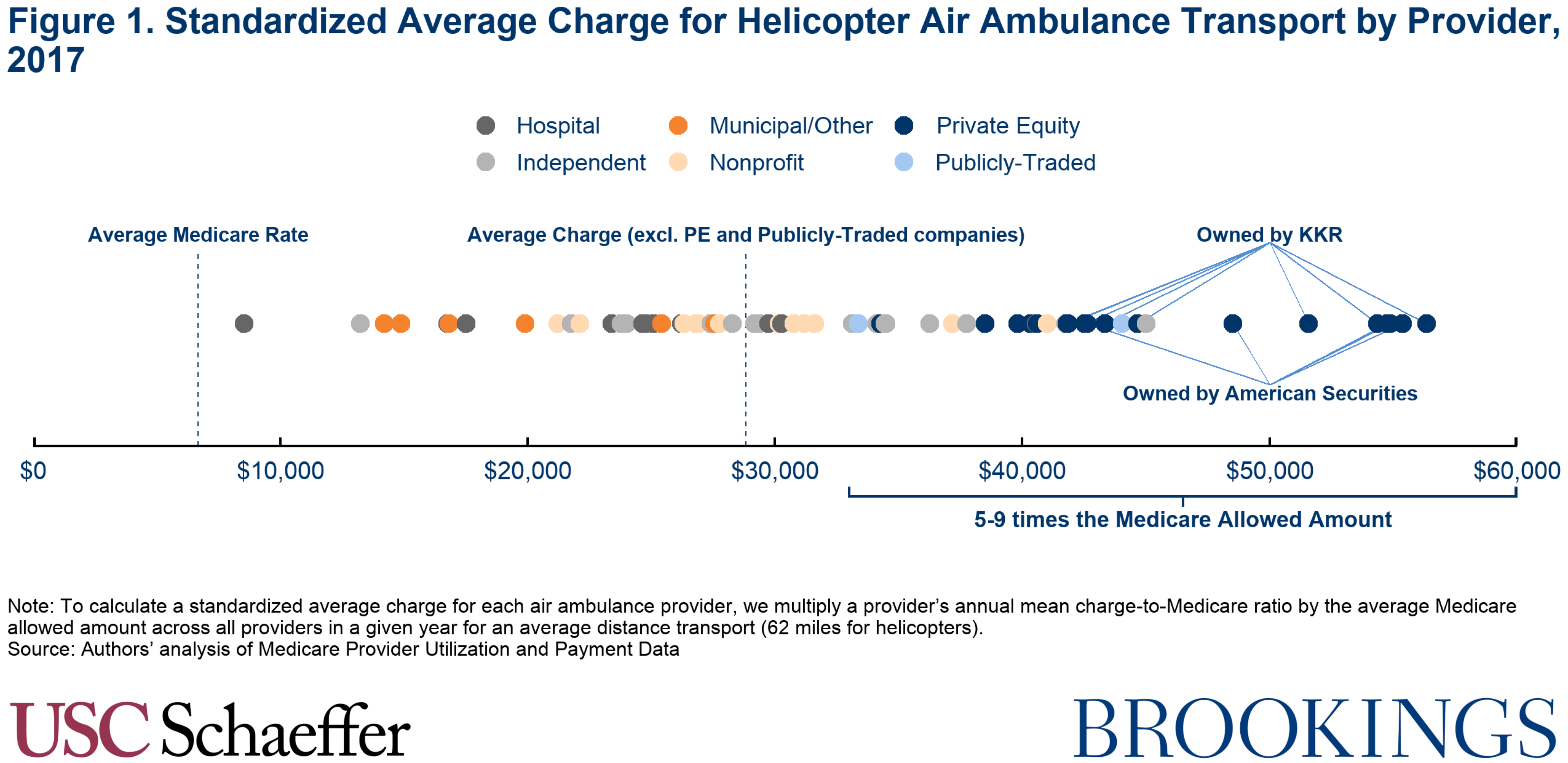

In 2017, we find that helicopter air ambulance carriers owned by two private equity firms, who together make up 64% of the Medicare market, had a standardized average charge of $48,250 (7.2 times what Medicare would have paid). This is markedly higher than the $28,800 (4.3 times what Medicare would have paid) standardized average charge for the same service by air ambulance carriers that are not part of a private equity-owned or publicly-traded company.

A similar phenomenon is also apparent in the fixed wing air ambulance market. Air ambulance carriers owned by the same two private equity firms, plus one additional small private equity-owned carrier, represent 62% of the Medicare market and had a standardized average charge of $58,750 (8.7 times Medicare prices), while other carriers charged an average of $38,200 (5.6 times Medicare prices).

Why Charges Matter

For providers that patients do not proactively choose, such as air ambulances or emergency physicians, charges – akin to a list price – play an important role in negotiations with health plans and can directly impact out-of-network patients who may be liable for the difference between the charge and what their insurer pays – a practice known as “balance billing.” The influence of charges is likely particularly pronounced in the air ambulance market because neither insurers nor patients are able to select a preferred carrier for non-interfacility transports. Indeed, one study found that nearly 80% of helicopter air ambulance transports for commercially-insured patients are out-of-network and that for half of these out-of-network transports, the insurer pays the full charge with no apparent correlation to the magnitude of the charge. While the insurer paying the out-of-network air ambulance operator’s full charge is helpful to the individual patient, these costs are typically reflected in higher premiums and can incentivize providers to set high charges. By comparison, roughly one-quarter of out-of-network professional service bills at in-network ambulatory surgery centers had their charges paid in full. The same study also found that in-network air ambulance prices averaged 80% of billed charges, which is substantially higher than in physician specialties.

Rapid Growth in Charges

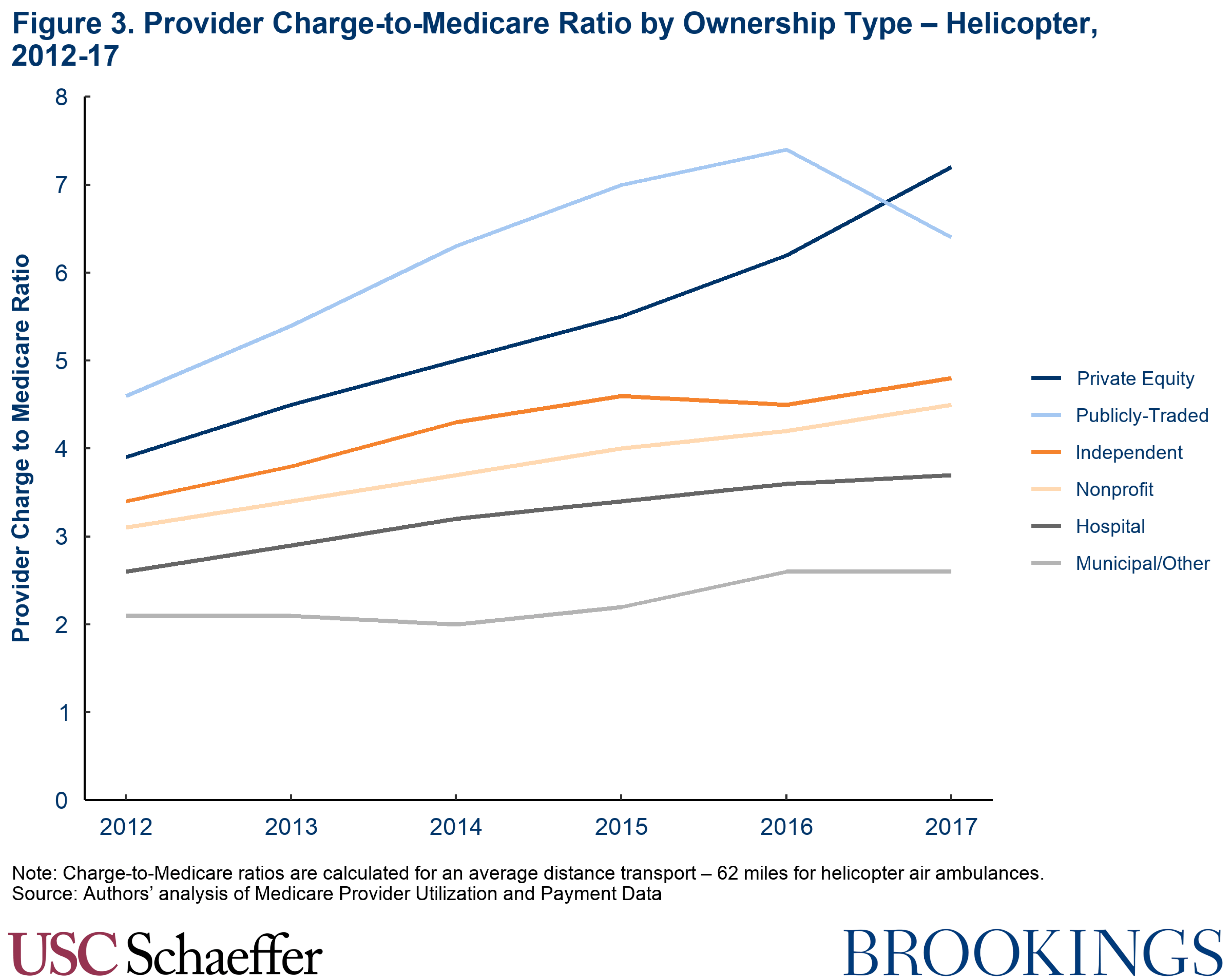

Previous studies have highlighted the rapid growth in air ambulance prices and charges, but the growth in charges (not just the level) has also been especially pronounced among private equity-owned carriers. Among helicopter providers, we find that standardized average charges from private equity carriers grew by 79% between 2012 and 2017 (an average of 12.4% per year), adjusted for inflation, compared to 36% growth for carriers not part of a private equity-owned or public company. Had private equity air ambulance carriers grown their charges at this lower rate, their standardized average charges in 2017 would have averaged $36,500 rather than the actual $48,250.

Consistent with this finding, we also note that GAO reported that Air Methods, a large helicopter air ambulance provider acquired by the private equity firm American Securities in 2017, indicated “that they have increased the average price charged per transport from $13,000 in 2007 to $49,800 in 2016—an increase of 283 percent over the past decade.”

While fastest for private equity-owned carriers, charge growth in the rest of the market is also notable. The 36% growth mentioned above amounts to annual real growth averaging 6.3% since 2012, far quicker than income growth or growth in most other health care prices. The highest-charging provider in 2012 had a standardized average charge of $39,500, less than the median standardized average charge of $41,900 in 2017. GAO also makes clear that this rapid growth did not begin in 2012, as they found average charges in the market doubled from $15,000 to $30,000 between 2010 and 2014. We estimate that the market-wide standardized average charge for a helicopter transport was $42,250 in 2017 (and $33,000 in 2014).

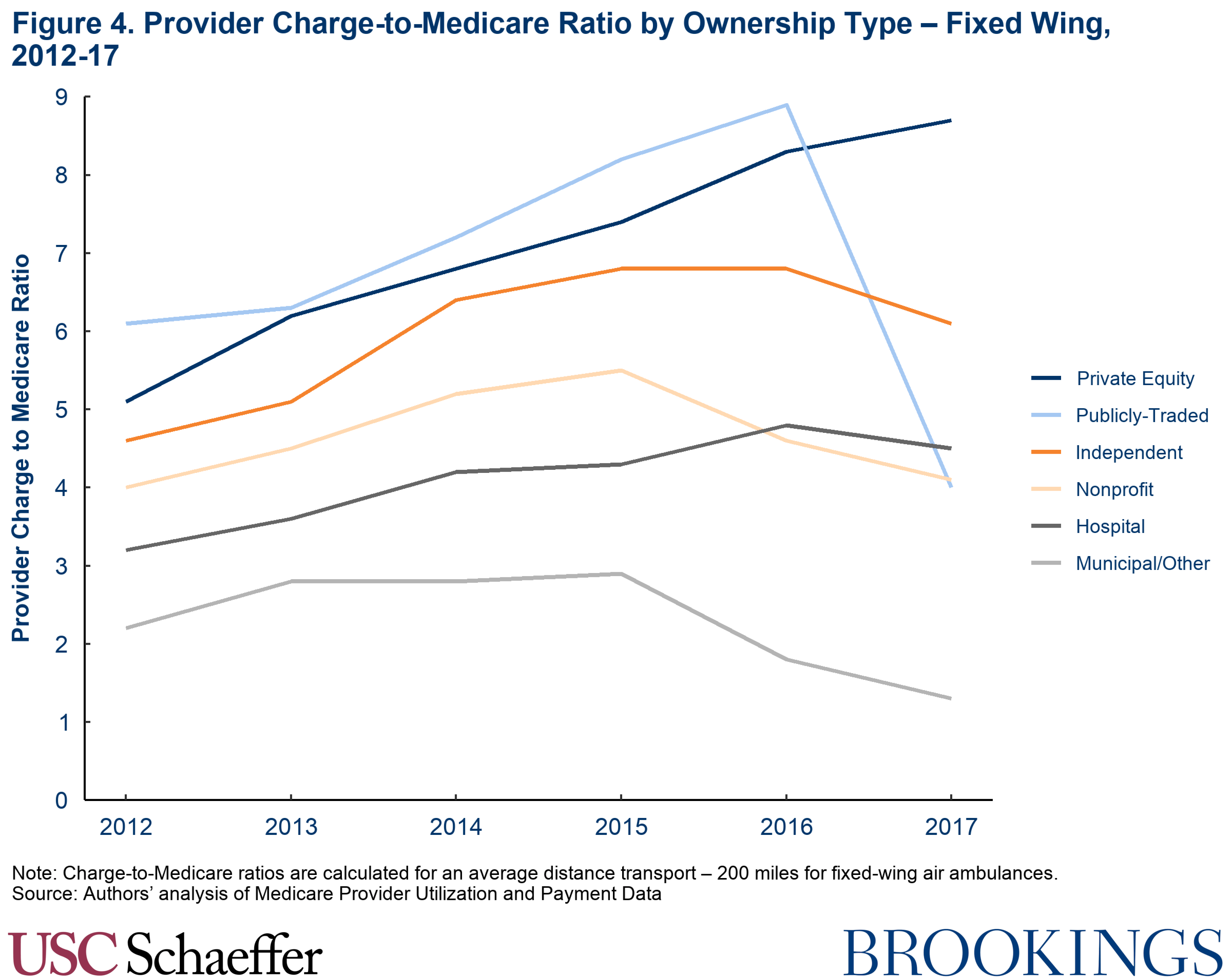

A similar dynamic is apparent among fixed-wing carriers. Standardized average charges from private equity operators grew by 65% between 2012 and 2017, measured in real 2017 dollars, in contrast to 19% growth among other providers. This differential growth translates to private equity fixed-wing air ambulance charges being $16,500 higher in 2017 than had their charges grown in line with other carriers in the market.

Private Equity Dominance of the Air Ambulance Market

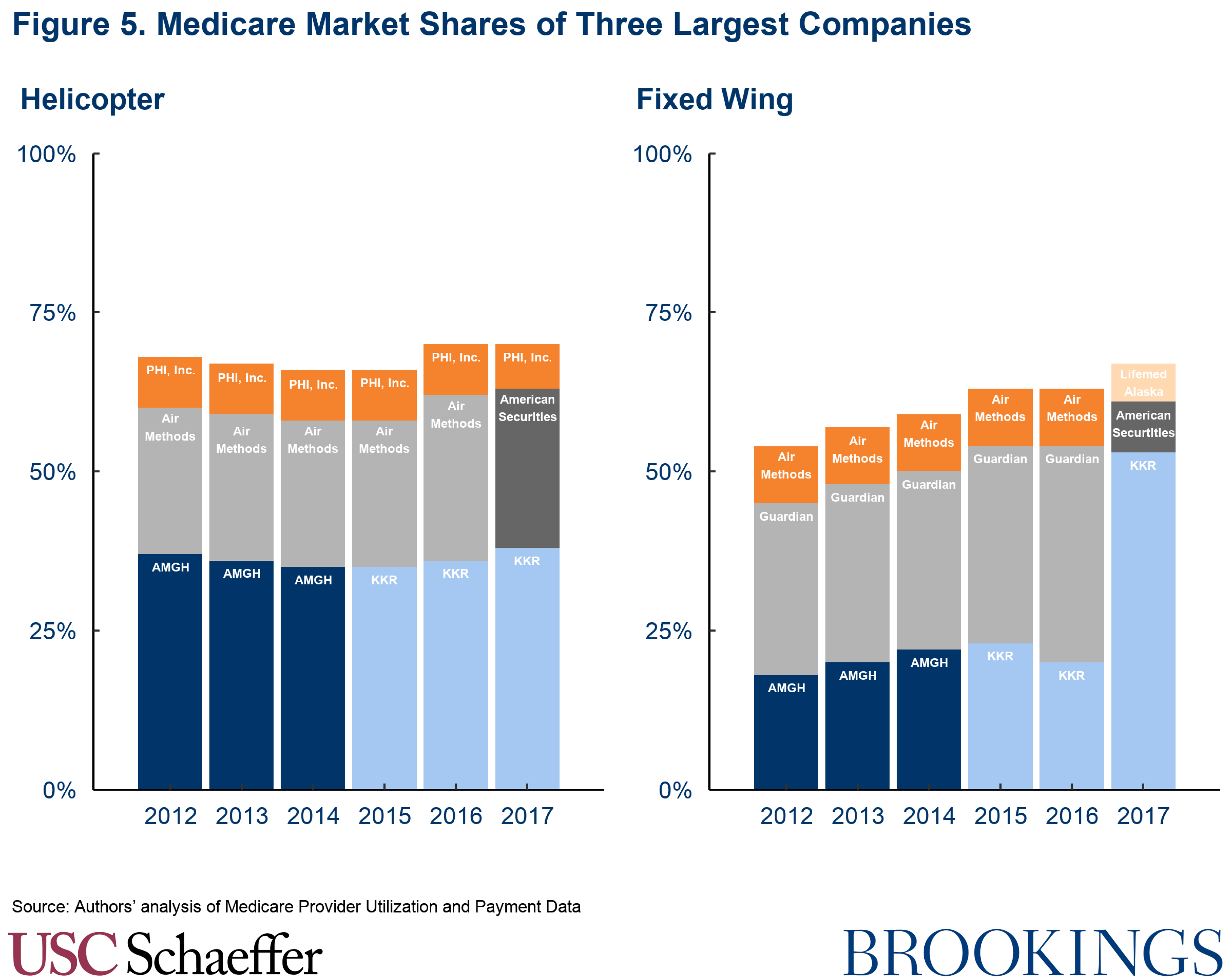

By 2017, private equity companies controlled nearly two-thirds of both the helicopter and fixed-wing air ambulance Medicare markets nationwide, buoyed by two large acquisitions that year – American Securities’ acquisition of Air Methods and KKR’s acquisition of Air Medical Resource Group. The latter purchase also represented a large consolidation of the fixed-wing market, growing KKR’s market share of Medicare services from 20% to 53%.

Discussion

Our findings add to the body of literature identifying high and fast-growing prices in the air ambulance market, and they illustrate that these trends are especially pronounced among private equity-owned carriers. It is plausible that quality differences may explain some of the differential pricing by ownership status, but any such differences seem unlikely to fully explain the very large gaps in charges across different carriers. Improvements in quality over time similarly seem unlikely to fully explain the rapid growth in charges across the entire air ambulance market, but especially among private equity carriers. Companies that operate air ambulances often attempt to defend high prices by citing what they consider underpayments by public payers. While not implausible, particularly for publicly-run carriers, empirical studies have consistently contradicted such “cost-shifting” claims in the context of hospitals. And again, even if true, it is hard to envision how changes over time in air ambulance payer mix can explain the extreme growth in prices and charges over the last decade.

More likely, certain market failures that characterize the provision of air ambulance services may help explain the high and rising prices. Air ambulance prices are less constrained by typical price competition than prices in other markets, given the common inability for patients or their health plan to select a carrier and that carriers can balance bill out-of-network patients. Increasing charges is also made more profitable by employers’ willingness to pay full charges for out-of-network provisions with seemingly little regard to the magnitude of the charge, likely due at least in part to the rarity of air ambulance services and the financial toll such a bill would place on an employee.

As a result, fixing the air ambulance market likely requires one of two approaches, discussed in greater detail in another paper. One option would follow a similar structure to proposals aimed at addressing broader surprise out-of-network billing, combining a prohibition on balance billing with a minimum payment requirement tied to a multiple of Medicare’s prices – which already include adjustments for geography and bonuses for pickups in rural locations. Bipartisan Congressional proposals released by the Senate HELP Committee, House Energy & Commerce Committee, and House Education & Labor Committee include a similar approach, although with the minimum payment requirement tied to current average in-network payment rates rather than a multiple of Medicare prices. The other option is to create a competitive bidding process to award contracts to different air ambulance carriers to cover different geographic regions, similar to a public utility regulation model.

Methodological Appendix

We utilize Medicare Provider Utilization and Payment Data: Physician and Other Supplier for years 2012-2017, a public use file published by the Centers for Medicare and Medicaid Studies (CMS) that summarizes Medicare payment and utilization data at the provider name / HCPCS code / year level. These data include information by provider on the number of services provided to Medicare patients, the average Medicare allowed amount for each HCPCS code, and the average charge for each HCPCS code. We identify air ambulance providers by the HCPCS codes they bill – A0430 and A0435 are the base pickup and mileage codes for fixed wing aircraft, and A0431 and A0436 are the same for rotary wing aircraft. We restrict our analysis to providers based in the 50 U.S. states and the District of Columbia.

We then construct a crosswalk identifying the parent company of each air ambulance provider utilizing company websites, Pitchbook, and press releases. If we are unable to identify a parent company, we assume that the provider name reported to Medicare is the parent company. Additionally, we identify whether each parent company is a private equity firm, a publicly-traded company, an independent company, a hospital, a non-profit (exclusive of hospitals), or a municipal government. Using this crosswalk, we then calculate market shares (among Medicare beneficiaries) and average charges for each parent company and ownership type, weighting by total Medicare allowed amounts.

To aid comparisons, we calculate a standardized average charge for each air ambulance provider in each year. To do this, we multiply a provider’s annual mean charge-to-Medicare ratio by the average Medicare allowed amount across all providers in a given year for an average distance transport (62 miles for helicopters and 200 miles for fixed-wing air ambulances). Medicare prices differ for rural versus urban pickups, so this standardization effectively allows comparison of provider charges assuming a consistent breakdown of rural versus urban pickups. In practice, this standardization has little effect on comparisons relative to a simpler comparison that only controls for the length of transport. For example, the average private equity charge for a standardized rotary-wing transport in 2017 was $48,241, while the average charge for an average distance non-standardized transport was $48,159. As a result, this methodological choice has little impact on our findings.

You must be logged in to post a comment.